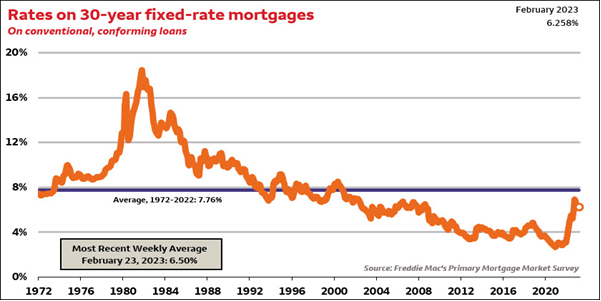

“We’ve never seen mortgage rates this high!” Never is a long time. While rising rates are a cause for concern for home buyers and sellers, alarm over current mortgage rates represents a rather limited view of historical patterns.

The average rate on a 30-year fixed rate mortgage climbed past 7% last November. More recently, mortgage interest rates are hovering around 6.5%. Regardless, current mortgage rates are a bit of a hike from the sub 3% rates we all enjoyed in 2021. What is surprising about rates, is that historically, rates above 7% have been the norm, not the exception. It’s only in the 21st century that we have seen consistent mortgage rates under 7-8%. Ironically, there is a whole generation of prospective home buyers who see mid-single digit rates as normal.

Locked-in?

Per a recent of analysis by Redfin of data (Q1 2022) from the Federal Housing Finance Agency, 62% of homeowners have a mortgage. Thanks to the refinance boom in 2020 and 2021, 85% of those mortgages are under 5%. That implies that if your transferee is a homeowner, it’s over 50% likely that they perceive themselves to be “locked in” to their current home given the additional monthly outlay required if they sell and buy into a higher rate mortgage. Assuming the percentage of homeowners without mortgages skews more toward retirees, the percentage of potential transferees locked into their currently mortgages is likely much higher then 50%.

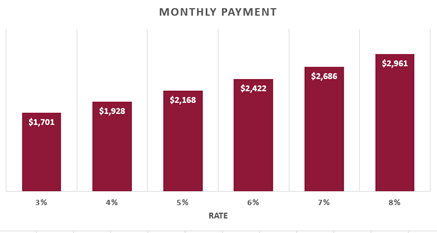

This chart clearly shows how transferees with mortgages below 5% can feel locked in to their current home. On a $400,000 mortgage, the difference between 3% and 7% is substantial, $985 per month for principal and interest.

What to do?

We could simply wait, and hope that rates come back down. But given the Fed’s focus on inflation, even if they pause the increases for a while, it’s unlikely that rates will come back to 3-4% range anytime soon.

We could ignore the issue. If employees want to take advantage of the opportunities available through relocation, they are just going to have to suck it up and pay the higher monthly amount. But given tight labor markets, this is probably not the strategy that will ensure employers meet recruiting and retention goals.

Fortunately, there are a variety of relocation benefit options which can help in the current environment. Let’s look at a few.

Points

Traditionally, lenders have always offered the option for the borrower to pay an extra point or two upfront, to get a lower interest rate over the life of the loan. For the past few years, with rates below 5%, points had fallen out of favor as the rate was already sufficiently low enough that additional outlays were unwarranted. Also, most relocation programs prohibit reimbursement for points as part of closing cost benefits. With a few caveats, on a conventional loan, you can expect a .75% interest rate reduction for one point, and perhaps 1.25% reduction with two points up front. This is the most direct approach. For a few thousand dollars, the employer can provide some relief to a transferee moving to a higher rate mortgage. Also, points will impact the payment for the life of the loan as opposed to temporary allowances or buydowns.

Temporary Buydown

A temporary rate buydown allows the borrower to pay a lump sum amount at closing to lower the interest rate, and the monthly payment, for a designated period — usually, 2-3 years. This helps the transferee ease into the higher monthly payment. In a two-year buy down, for example, the buyer’s interest rate would be reduced by two percentage points in the first year and one percentage point in the second year, reducing their payments for the first two years. In year three, the rate would go back to the note rate for the life of the loan.

Mortgage Interest Differential Allowance (MIDA)

A somewhat more targeted approach, the MIDA is designed to bridge the gap based on the true difference between the new rate and the old rate on the same balance. It is formula calculated to only kick in if the gap reaches a specified threshold. Like a buydown, it is designed to be temporary, two to three years to reduce the initial impact of the higher rate. For example, assuming a 2% interest differential to qualify and an old mortgage amount of $400,000:

• 3.00% Old Interest Rate (Conforming 30 Year Fixed)

• 5.00% New Interest Rate (Conforming 30 Year Fixed

• 2.00% Interest Rate Differential X $400,000 Current Loan Balance (Old Mortgage)

• $8,000 is the yearly mortgage interest differential (.02 x $400,000 = $8,000)

Payouts are made monthly and graduated to provide greater benefit in the first year and disappear after three years. Payout Example:

Year 1: $8,000 x 100% = $8,000 Total or $666.66 / month

Year 2: $8,000 x 50% = $4,000 total or $333.33 / month

Year 3: $8,000 x 25% = $2,000 total or $166.66 / month

Total Provided to Transferee in the 3-year period = $14,000

Many lenders will administer the program and direct bill the employer for the allowance, making it transparent to the employee. MIDA benefits cease if within the subsidy period, the employee: (1) terminates employment; (2) relocates again; (3) sells their new home; or (4) modifies or refinances the mortgage on their new home.

Policy Options

There are a variety of ways to combine these methods. An employer may also wish to create shorter or longer subsidy periods and/or create sliding scales based on degrees of interest differentials. We cannot predict where or how much rates will change in the future. Rather than creating firm policy benefits at this time, it may be best to address these benefits on a case-by-case basis, as an exception, rather than the rule. If you are running into these situations, reach out to your HomeServices Relocation Client Services VP for a discussion of alternatives.

HomeServices Relocations’ mobility policy management services are designed to help you spend time managing your business with confidence that your recruitment and retention goals are being supported by a professional and trusted relocation partner.

{kind=link}