The Tax Cuts and Jobs Act: Sunset or Reinstate?

Gary Conerly, CRP, GMS, Director of Client Advisement

The Tax Cuts and Jobs Act (TCJA), enacted in 2017, brought significant changes to the U.S. tax landscape, impacting various sectors of the economy, including the relocation industry

The TCJA introduced several key changes, such as adjustments to individual and corporate tax rates, modifications to deductions, and alterations in international tax policies. These changes had significant impact on shaping relocation policy decisions and strategies in regard to employee relocation tax.

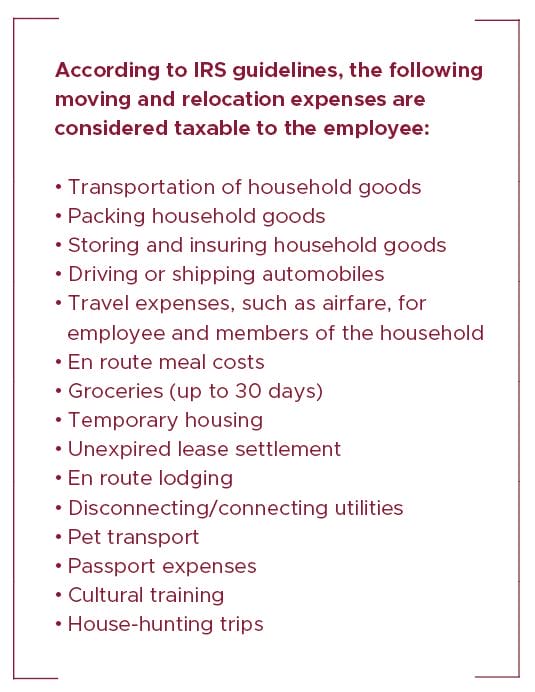

The most significant impact on the relocation industry was the elimination of moving expense deductions. Prior to 2018, qualified household goods moving expenses were not treated as income to a relocating employee and therefore not taxable.

The Tax Cuts and Jobs Act took effect on January 1, 2018, and is scheduled to sunset in December 2025. It suspended this exclusion and now requires employers to include moving related expenses as taxable income in employees’ wages. It does not matter if an employer chooses to provide a lump sum payment, a reimbursement to the employee, or make a payment directly to a moving company or relocation management company. The expenses are taxable to the employee.

Understanding the effects of the Tax Cuts and Jobs Act sunset provision in 2025 is vital for informing employee relocation programs, as changes in tax policy can significantly influence corporate decisions regarding workforce mobility, investment strategies, and talent recruitment efforts.

The sunset provision and its impact on the relocation industry

With the TCJA sunset provision looming in 2025, there is growing uncertainty about how the industry will be affected. Without Congressional action, 23 different provisions of the 2017 TCJA are set to expire after 2025, including taxable employer paid moving expenses for relocating employees. If no new laws are enacted, the taxable nature of these expenses will revert to pre-2018 status—which means paid relocation expenses would no longer be classified as ordinary income.

The Worldwide Employee Relocation Council (WERC®), the governing association for the global mobility industry, and the Moving & Storage Conference of the American Trucking Association (ATA), along with the International Association of Movers (IAM) have formed a formal effort, the Relocation Mobility Coalition, 1 which is advocating for the reinstatement of the moving tax deduction. The Coalition seeks to collect pertinent data and provide outreach tools for the mobility industry to show support for reinstating tax deductions for relocating employees.

At this point, the road ahead is unclear. In February 2023, House Republicans reintroduced the TCJA Permanency Act which would extend the Tax Cuts and Jobs Act beyond December 2025. While it is unlikely that Congress will take any action in 2024, if the TCJA is renewed or made permanent in 2025, then employers will be required to continue including moving related expenses in

their employees’ wages. House Republicans oppose the renewal of the TCJA.

The TCJA influence on employer-sponsored relocation decisions and practices

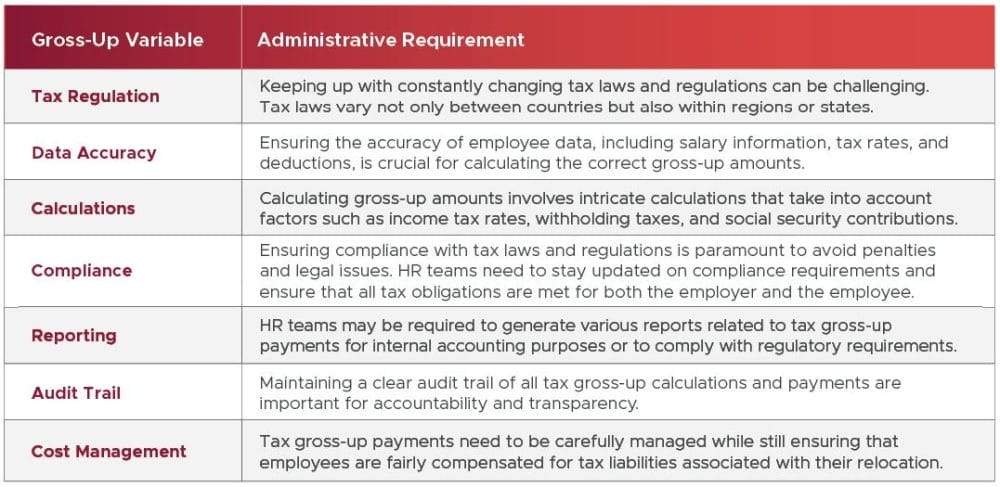

The tax shift imposed by the TCJA has altered the dynamics of employee relocations for both employers and employees. Smaller relocation budgets, higher out-of-pocket costs for employees and a competitive job market have prompted many employers to provide a gross-up on their moving-related cost expenses to cover the additional taxes incurred by the employee. Although the gross-up calculation solves employee relocation tax issues, it creates additional administrative burdens for HR teams and additional cost for employers seeking to fill open positions or grow their company.

Shortly after the TCJA took effect, Worldwide ERC® conducted a member survey regarding the number of organizations implementing relocation program/policy changes as a result of the new tax laws.2 The survey responses suggest that the industry is adapting to changes, with most companies continuing to move employees and gross them up for taxable costs but adjusting to some extent either the number of relocations or the scope of benefits to maintain control of costs.

The role of Relocation Management Companies in managing gross-up calculations

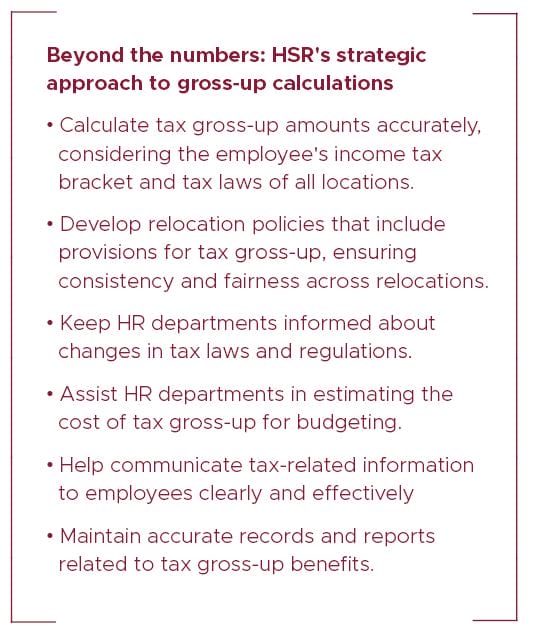

Relocation Management Companies (RMCs) can be a great resource in ensuring your relocation policy keeps pace with market fluctuations, technology and business regulations. HomeServices Relocation helps HR departments by providing expertise and support in navigating the complexities of relocation-related tax regulations. As relocation services have become more complex, few in-house personnel are experts on all facets. Consequently, outsourcing relocation has become critical as companies look for ways to reduce costs while maintaining a competitive edge to attract key talent.

HomeServices Relocation routinely provides benchmarking and policy recommendations to our clients resulting in tangible program improvements and cost savings. We have witnessed the impact of these service enhancements and savings year after year as our recommendations were fully implemented.

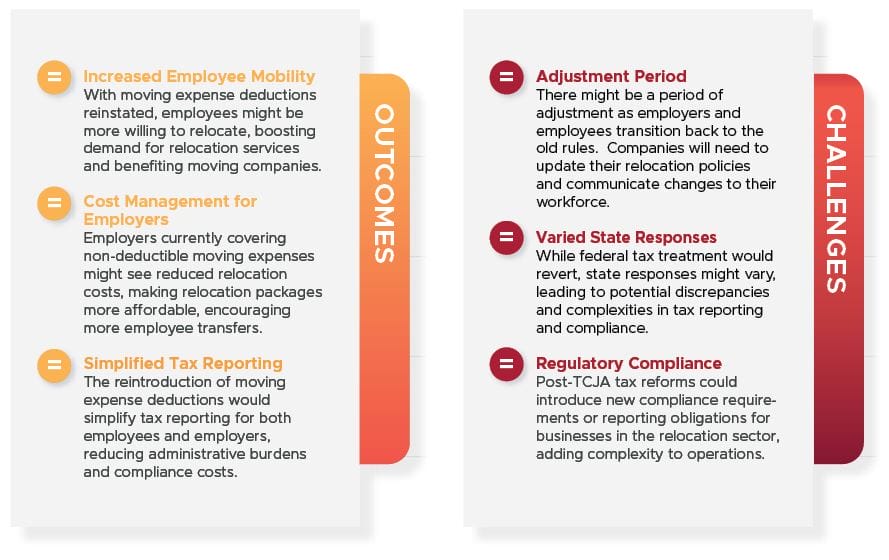

Sunset: Outcomes and Challenges

If the TCJA sunsets, the tax classification for an employee’s moving expenses would revert to pre-2018 rules. This means that employers would no longer need to gross-up moving costs and other relocation related expenses (costs incurred by the employee during their final trip to destination).

These outcomes and challenges highlight the implications of TCJA sunset on the relocation industry, emphasizing the need for proactive planning, policy advocacy, and strategic adaptation to navigate potential challenges and opportunities.

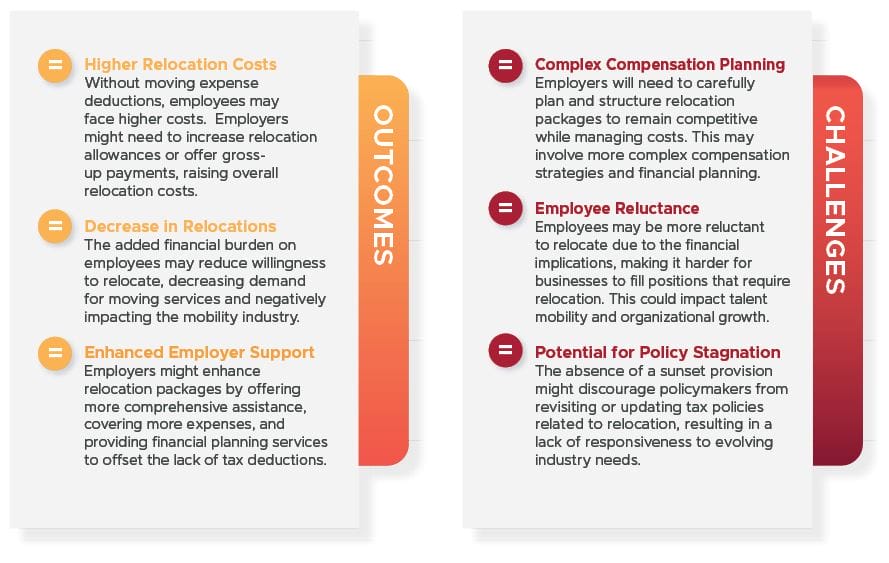

Reinstate: Outcomes and Challenges

If the TCJA is reinstated, the current rules will continue, where moving expenses are not deductible for most employees. Employers who wish to cover these costs must classify the expense as taxable ordinary income to the employee.

These outcomes and challenges highlight the potential implications of retaining the Tax Cuts and Jobs Act beyond 2025 on the relocation industry, highlighting the balance between stability, benefits, and potential challenges that stakeholders in the industry may face.

Recognizing tax changes that affect your bottom line

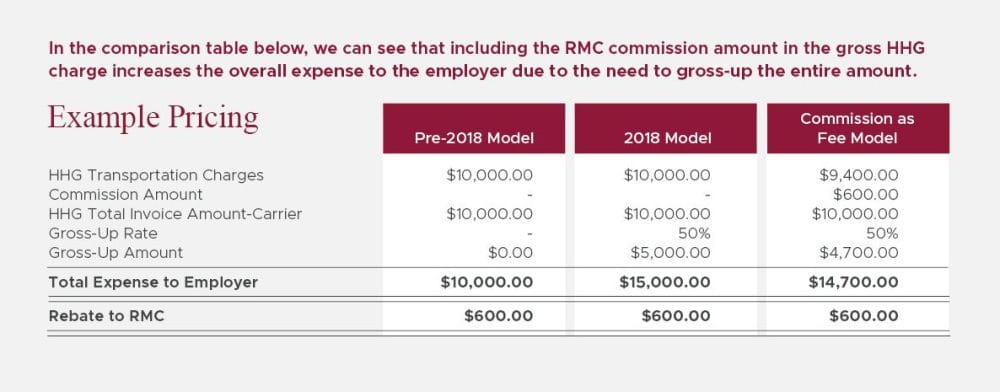

A side effect of TCJA is increased awareness of how the relocation industry generates revenue. For decades it has been a common practice for a relocation management company (RMC) to, in some form or fashion, earn a “commission” or “rebate” paid by the moving company to their organization. Another tactic commonly employed is to not pass along the full discount negotiated with moving companies and other suppliers. These commissions are paid from the carrier to the RMC as rebates after the fact, with the commission amount embedded in the total invoice billed to the employer. The commission is part of the overall fee structure the client pays to the RMC for outsourcing the mobility function.

Fees paid to RMCs for services are not considered taxable income to the employee but are treated as business expenses. As a business expense, fees are not subject to gross-up, saving the employer additional tax assistance expenses. Unfortunately, with HHG expenses now taxable, the portion of the invoice which represents the fee is also now taxable, unnecessarily increasing gross-up expenses for the employer.

In 2018, HomeServices Relocation implemented invoicing process changes to reclassify commission rebates earned on taxable items as fees, affecting household goods, storage, auto shipment, temporary lodging, and family assistance. By classifying these rebates as fees, we can reduce the taxable amount imputed to the transferee, reducing gross-up expenses to the employer. Savings are projected at over $1M per year across our entire client base. We are leading the industry in this regard and first to market with advising clients of this cost-saving opportunity.

HomeServices Relocation is unique in the mobility industry in that, other than for real estate and mortgage, no revenue is received from any of our providers. This ensures that our clients get the lowest overall cost and that our clients avoid paying unnecessary gross ups due to inflated pass-through costs. Our TruePartner® pricing program ensures unbiased procurement decisions that align with relocation program goals for cost and service.

HomeServices Relocations’ mobility policy management services are designed to help you spend time managing your business with confidence that your recruitment and retention goals are being supported by a professional and trusted relocation partner.

{kind=link}